- News

- Business News

- India Business News

- How to fix your money problems

Trending

This story is from March 9, 2020

How to fix your money problems

Whether you are a single woman or sandwich mom, find out how to meet the financial challenges that impact your savings and future.

")

(Representative image)

(This story originally appeared in  on Mar 2, 2020)

on Mar 2, 2020)

NEW DELHI: At best, it is an uneasy relationship. At its worst, the relationship doesn’t exist. It may be easy to blame years of social conditioning and patriarchal traditions for the unhappy bond between women and money, but it’s time women learnt to make peace with it. Despite the financial pitfalls that a woman encounters at work and home, it is a good time to take charge of her finances. on Mar 2, 2020)While there is a greater need for a change in work culture and cooperation from family members, there are several steps she can take to empower herself financially.

With easy access to online information, changing social norms, as well as the freedom to earn and invest, women need to shrug off the taboo and meet the financial challenges head on. Start this Women’s Day!

Earn less, save more

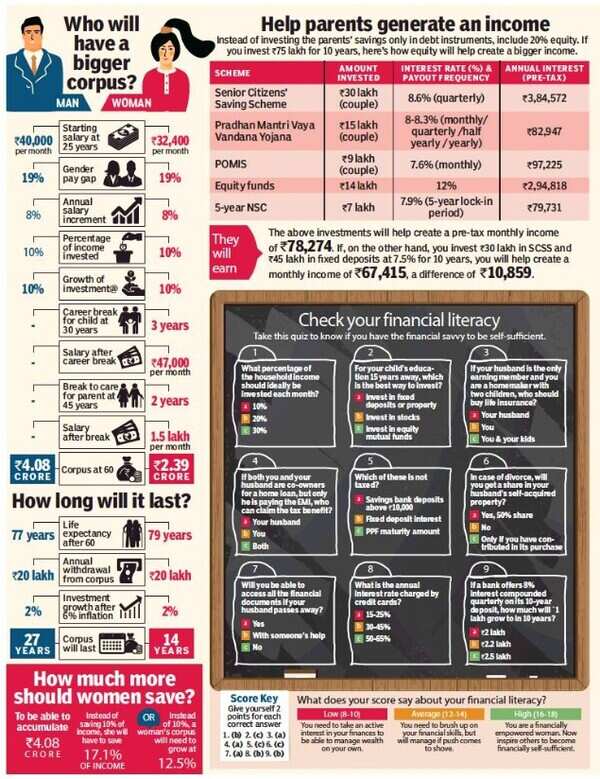

Single women, be it a mother, divorcee or widow, struggle to manage finances because they are hampered by three hurdles: gender pay gap, caretaking breaks that disrupt their careers, and a longer life span, with a life expectancy of 78.6 years at 60, compared with 77.2 years for men.

Given that there are nearly 74 million single women in India as per the 2011 Census, it is imperative that they learn how to secure their finances better.

Gender pay gap: According to the Monster Salary Index Report 2019, women in India earn 19% less than their male counterparts, with the median gross hourly salary for men being ₹242.49 in 2018, compared with women, who earned ₹196. “At the executive level, the gap is 45%, while it is lesser at 20-35% for entry level,” says Anjali Raghuvanshi, Chief People Officer, Randstad India. What this means is that for similar work, skills and experience, a man will earn more.

Career breaks: When it comes to caretaking, be it for kids or sick parents, it is women who take a break from their work lives. “So, not only is there no linear career progression for her, but she also loses retirement benefits and forced savings in EPF and VPF,” says Priya Sunder, director, PeakAlpha Investments. The disruption in salary also means that she stops investing.

Combating hurdles

There are various ways a woman can be proactive about reducing the pay gap.

Don’t stop networking: “She needs to continue to network with colleagues and other people in the industry,” says Neeti Sharma, senior vice-president, Team-Lease Services. If she rejoins after 2-3 years, she may not be able to join the same firm so she should remain connected with people in the same line of work.

Invest in your skills: “Even if she rejoins after the mandatory six months of maternity leave, she may want a different work profile,” says Raghuvanshi. So it is important to keep upskilling and updating with the latest developments.

Negotiate better: There is nothing wrong in asking for rewards and equal pay if your performance is at par with your male co-workers.

Strategies to raise savings

Speed up saving: Since the woman will end up saving less due to the gender pay gap and fewer years she puts in at work, one way of overcoming this hurdle is by increasing her monthly savings. So if a 25-year-old woman is building a corpus for retirement at 60, she will have to save nearly 17% of her income compared with 10% that men would have to in order to build the same corpus. If she finds it hard to do so, she can automate her investments or raise the EPF and VPF contribution with her employer, so that the money is saved before she can spend.

Optimise investments: Though there is no difference in the way a woman or man invests, the best way to make up for lost time and money is to invest smarter. For long-term goals, be it retirement or her children’s education, which are more than 12-13 years away, she should harness the growth of equity, which gives one of the highest returns in all asset classes. A small portion, however, needs to be kept in debt for safety.

Protect investments: A single woman should stock up at least eight months of household expenses as contingency corpus. To protect her kids, buying term life insurance, which is 7-10 times her annual income, is important. To avoid medical costs eating into her retirement corpus, she should also buy health insurance for herself and her children.

Work longer: She should enhance earning power and compensate for lost money by skilling herself so that she continues to work even after retirement.

‘Sandwich’ moms

Despite being consummate jugglers, women may not always relish being a ‘sandwich’, caught between the financial needs of their parents and kids. However, prioritising needs and optimising investments can help.

Secure yourself first

From the day you start earning, invest for your retirement by putting your money in a mix of equity funds and debt instruments. If you are in your 30s, put at least 70% of your savings in equity and 30% in debt. The former can be in the form of equity funds and the latter can comprise EPF, VPF, PPF and NPS.

Another tool to secure your family is to buy term life and health insurance. For health, pick a ₹5-10 lakh family floater plan for your spouse and kids, but buy a separate plan for your parents. Also take a ₹25-30 lakh critical illness plan for yourself and your spouse.

How to help parents

If your parents do not have a regular income stream, it’s likely that you will end up supporting them and compromising your own goals. What should you do? “It is rare that parents don’t have money. It’s just that it is illiquid, and in the form of property or gold,” says Sunder.

So the first step is to monetise these assets as it will offer financial independence to your parents and reduce your burden. Help invest their corpus in debt instruments, with a 15-20% equity component to help the money grow. If you are working, cover your parents in the group policy. If you are not employed, buy a small base cover for parents and a higher top-up plan with a deductible.

Children’s needs

Since the child’s goals are for the long term, invest in equity funds via systematic investment plans (SIPs), which will give good returns in 15-16 years. With soaring education inflation and the pressure of saving for their own retirement, parents no longer have the luxury of funding both the education and weddings of their children. So they must focus only on the education goal, even take an education loan if required, and let the kid fund his own wedding.

Financial literacy

Nearly 80% of Indian women are illiterate compared with 73% men, according to the Standard & Poor’s Ratings Services Global Financial Literacy Survey 2015. While most women manage the household and take smaller financial decisions, the bigger decisions are typically left to the males. This low engagement in financial processes results in heightened risk in case of divorce or death. Another reason is the deliberate exclusion of woman from financial matters by men to retain an upper hand. Instead of being offended, women should continue to ask questions, read up and make every effort to know money better.

What to know

What you need is a working knowledge of financial instruments so you can invest and reach your goals. Also try to read about basic concepts like inflation, interest rates, loan EMIs, and enable yourself to conduct basic Net banking operations and simple mathematical calculations. Understand the purpose of different types of insurance and how much you should have to protect yourself and your family.

Become financially literate

Take the first step: Despite the conditioning and societal bulwarks, all that a woman needs to do is take the first step. Beyond managing the household budget, she should invest the money herself, even if it’s in the simplest instrument. Watching the money grow will give her a sense of empowerment and freedom.

Financial literacy apps: Use apps like Meri Dukaan, Financial Literacy, and Financial Education Books, to educate yourself about personal finance.

Watch videos on Youtube: This is the simplest way to understand basic concepts like inflation, growth and equity. These are readily available and will explain to you the complex processes in an easy language and a simple manner.

Read up on basics: Try to avoid electronic media while taking the first learning steps because you could end up becoming more confused. But do read newspapers and books, starting with primers on banking, mutual funds, etc.

Employer workshops: “You should take every opportunity to attend your company’s financial skilling programs under the CSR initiative,” says Sharma. Don’t hesitate to ask questions and try to apply the learning to your finances.

End of Article

FOLLOW US ON SOCIAL MEDIA

Hot Picks

TOP TRENDING

Trending Stories

In Business

Entire Website

- Will banks open only for 5 days a week? Here’s what you should know about IBA’s proposal

- India set to be third largest economy, says S&P Global

- Dalal Street bull run continues! BSE Sensex crosses 69,000 for the first time; Nifty above 20,800

- Byju’s reduces notice period for employees as troubles mount

- Sensex surges over 900 points, Nifty above 20,550 as BJP state election wins bolster Modi's Lok Sabha 2024 prospects

- UltraTech to buy building materials business of Kesoram in 7,600 crore deal

- Tata Technologies stock debuts at a bumper 140% premium; share price at Rs 1200 on BSE

- Tata Technologies share allotment: How to check IPO allotment status, listing date, GMP

- BSE m-cap rides rally in Adani stocks, tops $4 trillion

- Charlie Munger, who helped Warren Buffett build Berkshire, dies at 99

- J&K assembly elections: Strong emotions over Article 370 unite youths in Valley

- CM-designate Atishi meets Kejriwal ahead of oath-taking ceremony

- Animal fat in Tirupati laddu: Why lakhs of devotees are outraged

- 'Married to Pak ...': Kharge's jab at PM over remarks on NC-Cong tie-up in J&K

- 1st Test Live: Ashwin grabs three as Bangladesh falter

- Girl hit by vehicle while riding scooter, ends up stuck on pillar

- Why investors must keep an eye on rising promoter stake sales

- EY employee's death: Anna Sebastian's father appeals to the company

- 'There are two batters in India...': Ex-Pak player hails Pant

- Amul files complaint against 'misinformation campaign' linking it to Tirupati laddoos row

Popular Categories

Hot on the Web

Top Trends

Trending Topics

Daughter's Day WishesParvin DabasAbdu RozikMukesh KhannaJayamSana Khan HusbandTirupati Laddoo ControversyGOAT CollectionVaazha OTT ReviewKozhipannai Chelladurai ReviewCheetahsKangana RanautAditi Rao HydariDalljiet KaurHoliday DestinationVikas SethiBest Selling Earbuds Under 1000Apple iPhone 16 ProVirat KohliWordle Answer

Living and entertainment

Latest News

Stuck in Lebanon for 23 years, Punjab man back homeWhat is the 30-30-30 weight loss method? How to do it for maximum benefits?Supreme Court questions change in NEET-PG pattern, seeks response of NBE and CentreYudhra box office collection day 1: Siddhant Chaturvedi and Malvika Mohanan starrer opens with Rs 4.50 croreUP man kills newborn daughter in fit of rage over fourth girl cild, ArrestedSalesforce to expand its innovation hubs in Bengaluru, HyderabadThe truth about sugar substitutes: Safe alternative or hidden health risk?Return to office, student influx cause rents to soarMemeFi daily codes for 21 September 2024: Boost your earnings with daily codes and know how to maximizeRohit Sharma gets angry at team-mate: 'Soye hue hain sab log''One nation, one mom': Congress takes dig at viral Tirupati laddu tweets amid prasad rowWomen turnout exceeds that of men in six J&K seats in Phase-1Kate Middleton uses this parenting strategy to keep her kids disciplinedKarnataka CM Siddaramaiah signals probe into land case involving HD Kumaraswamy, BS YediyurappaVantika Agrawal's victory helps India draw against USA at the Chess Olympiad'Hiding among civilians': Israel reveals how IDF eliminated top Hezbollah commanderTrain mishap averted after fishplates, keys found on tracks in SuratBTS' Jin, ASTRO's Cha Eun Woo, and Kang Daniel claim top spots in September's K-Pop Idol Brand Value Rankings

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service